Financial well-being dips for U.S. adults in August

Here’s how worries about money are affecting different demographics in the second half of 2021.

In no uncertain terms, U.S. adults are worried about their financial future.

However, these fears are not equally felt across all populations. Older demographics, such as baby boomers, and high-income earners are more likely to report stable financial wellness scores. However, for others, August saw a drop in confidence for their personal economic fortunes.

For business leaders, the data is a warning against seeing one’s own financial resilience as a stand in for the feelings of workers across your organization. Employees at the bottom of the pay scale are shown to have diminishing faith in economic recovery and stability going forward, driven by the ongoing effects of COVID-19 and the Delta variant.

What questions should you ask?

To learn how your own workforce is responding to the ongoing pandemic crisis, leaders must survey employees and create opportunities for feedback. The Morning Consult report offers some examples of questions to ask that can demonstrate financial well-being or lack thereof.

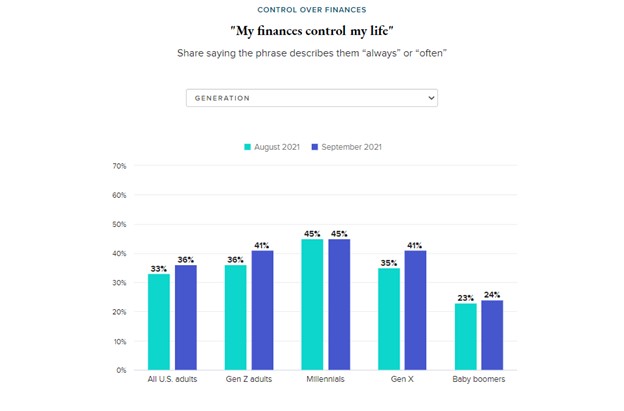

For example, asking respondents if the phrase “My finances control my life” can offer insight into how stressed workers are about their money. If workers say their finances are in control—as opposed to themselves—it indicates they feel out of control or helpless to address their situation.

Another question to ask employees is whether they could easily cover an unexpected expense.

After the data is collected

Once you have your answers, it’s crucial to have an action plan to address the results. Listening sessions and fact-finding missions that don’t lead to tangible company action can undermine trust with employees.

So, how can you build a financial wellness program that works? State Street Global Advisors has published a whitepaper that identifies six important steps:

- Understand the financial landscape. Map out the financial ecosystem for your employees and ask the questions as modeled by Morning Consult’s report.

- Define financial wellness for your organization. Financial security goes beyond income and assets. What knowledge and skills do you want your employees to have? What outcomes are you looking to achieve for your workforce?

- Lean on best practices. Financial planners and advisors have a wealth of research about the behavioral science behind financial decisions. Make sure your programs offer incentives that have been identified to lead to desired outcomes.

- Explore established and emerging solutions. Financial wellness for your organization might come with other tools than a retirement plan. Do you offer financial counseling or investment education?

- Overcome challenges. There is always resistance to change—and that will also be true when trying to change the financial stability for employees. Communications challenges, employee engagement issues and other roadblocks could threaten your entire wellness program. Experts advise to start small and build towards your goals incrementally with constant reinforcement and communications follow-up.

- Build a business case. If business leaders don’t see the financial upside for your organization, investment in employee wellness programs will falter, or fall off the radar completely. Important data points to measure include absenteeism, turnover, job performance, retirement readiness of employees, employee debt levels and more.

Check out the full data from Morning Consult on the current picture of financial well-being in the U.S. here.